How a consented structure with no flat plan update turned a dream home into a walk-away.

Sam and Mel found a cross-lease property they liked.

Three bedrooms, decent section, and a glass conservatory off the living area that caught the afternoon sun.

The listing price sat in the mid-$900,000s and they were ready to move.

There was one problem.

The conservatory had been consented by council, but it was never added to the cross-lease flat plan.

What a Defective Flat Plan Means

On a cross-lease title, the flat plan is the legal document that defines what the owner actually owns.

It shows the footprint of the flat, the exclusive use areas, and the common property.

If a structure does not appear on the flat plan, it falls outside what the title says belongs to the owner, regardless of whether council issued a building consent for it.

The listing floor plan clearly showed the conservatory attached to the upper floor (4.08m × 2.25m).

But the cross-lease flat plan registered at LINZ told a different story.

The conservatory sat outside the registered flat plan outline entirely.

Council Said Yes, the Title Didn't Follow

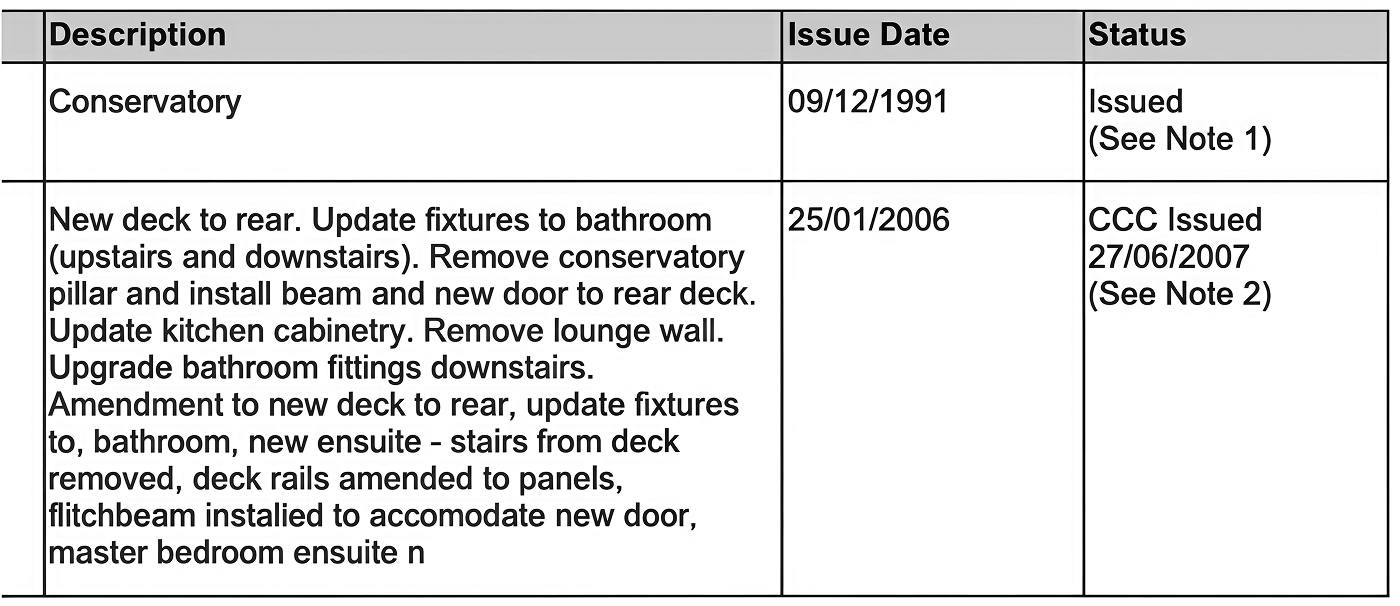

The LIM showed a building consent for the conservatory issued on 9 December 1991.

Council had no issue with the build.

But the cross-lease memorandum requires the written consent of all other lessees before any structural alteration.

An enclosed, attached conservatory is a structural alteration.

The flat plan was never updated to reflect it.

How We Worked Through It

We walked Sam and Mel through our cross-lease assessment flowchart to confirm the position:

We were direct with them.

If they bought the property with the flat plan as it stood, the defective title became their responsibility.

When they eventually sold, they would need to either fix it or disclose it.

Future purchasers would face the same hurdles: bank approval against a defective title, and insurer confirmation of cover.

Both are real obstacles that reduce purchaser interest and affect sale price.

Ask the seller to correct the flat plan before settlement as a condition of the agreement.

That would require the seller getting the neighbour's written consent and engaging a surveyor to update the plan at Land Information New Zealand.

Estimated cost: $10,000–20,000.

Sellers are often reluctant because of the expense and the delay.

Buy the property as-is and fix the flat plan after settlement, factoring that cost into the offer price.

Before doing this, Sam and Mel would need their bank and insurer to sign off on the defective title.

That sign-off is not guaranteed.

They would also need to confirm the neighbour was willing to consent, because without written agreement the update cannot proceed.

A third option existed in theory: demolish the conservatory and return the flat to its original footprint.

That would resolve the title defect without updating the flat plan, but it meant losing the room they liked most about the house.

Sam and Mel decided to walk away.

The unknown cost of fixing the flat plan, combined with the uncertainty around bank and insurer sign-off, made the risk too high.

They moved on to other properties.

When your client is buying a cross-lease property, the flat plan is one of the first documents to check.

If there is any structure on site that does not appear on the plan (a sleep-out, a carport, an enclosed deck, a conservatory), that is a red flag.

The client's lawyer will need to assess whether the title is defective and what it will cost to fix.

The earlier this is identified, the better.

If it surfaces after finance is approved and conditions are going unconditional, the options narrow and the pressure increases.

Flag it early, and your client can make an informed decision about whether the property is worth the extra cost.

For more on how cross-lease flat plan issues work, read Volume #40 of our knowledge base.

✔ On a cross-lease title, if a structure is not on the flat plan, it falls outside what the title says the owner owns — regardless of council consent.

✔ The conservatory had a 1991 building consent but was never added to the flat plan.

That made the title defective.

✔ Options: require the seller to fix before settlement (~$10,000–20,000), buy as-is and fix later (needs bank and insurer sign-off), or demolish the structure.

✔ Sam and Mel walked away.

The uncertainty around cost and sign-off made the risk too high.

✔ For brokers: check the flat plan early on any cross-lease purchase.

If any structure on site isn't on the plan, flag it before conditions are lifted.

✔ Read more: Volume #40 — Cross-Lease Flowchart