How I negotiate tricky building report issues, so they are fixed by the seller before the settlement day

In this edition, I'll explain how to handle tricky building report issues, so they are fixed by the seller before settlement day.

Here’s what we’ll cover:

This newsletter will not cover:

My client’s building report came back clear apart from one thing...

The kitchen floor was sloped beyond the NZ Building Code minimum requirements.

This meant the property was uninsurable and it was going to prevent my client from getting finance.

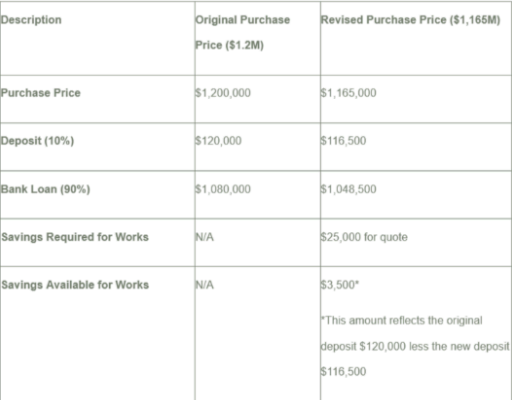

The repair quote was $25,000.

We shared this with the sellers and requested the kitchen floor should be re-levelled as a settlement requirement.

A settlement requirement means this now becomes a trigger for settlement to occur, similar to how title issuing can trigger a settlement for a new build property.

The sellers countered with a $35,000 price reduction.

New price $1,165,000.

My client was ecstatic and wanted to accept this.

I advised against accepting the reduction:

1. Lender Approval: The lender would need to sign off on this reduction.

2. Money for Repairs: My client had a low LVR and no savings for the repairs.

Without additional lending, the repairs would become his problem when he sold the property, likely worsening by then.

Price reductions might seem exciting but often lead to future headaches.

If your client buys a property with an issue, it will remain an issue (likely worsening) until fixed.

This often takes time and money.

Being Too Casual

Verbally agreeing with the seller to “get it fixed before the settlement day” is a recipe for disaster.

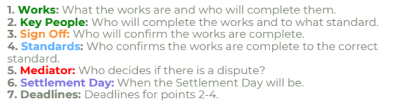

We need written agreement on who does what, by when, to what standard, and who provides the final sign-off.

Fixing something becomes increasingly complex because we need to consider:

Please refer to the Below Example to see how we have incorporated the above structure - we have colour coded the above requirements in our Example Below.

The negotiations and drafting took several rounds, extending beyond our original scope of instructions.

We provided an estimate for the additional legal work required.

For the one-and-a-half hours of extra-legal work, the process flowed smoothly, and my client received full insurance and lending for their re-levelled floor.

Despite the increased legal bill, my client was thrilled with the outcome: the work was done correctly, and they avoided the burden of fixing an uneven floor without savings.